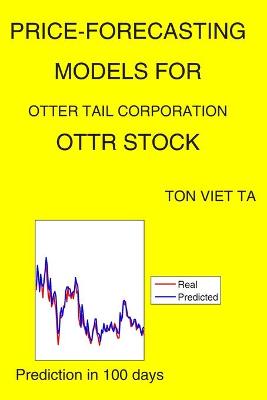

Price-Forecasting Models for Otter Tail Corporation OTTR Stock (NASDAQ Composite Components, #1967)

by Ton Viet Ta

Rigorous mathematical finance relies strongly on two additional fields: optimal stopping and stochastic analysis. This book is the first one which presents not only main results in the mathematical finance but also these 'related topics' with all proofs and in a self-contained form. The book treats both discrete and continuous time mathematical finance. Some topics, such as Israeli (game) contingent claims, and several proofs have not appeared before in a self-contained book form. The book conta...

Daghandel Med Central Pivot Range (Cpr), Volymviktat Rörligt Medel, Adx & Vortex Indikator

by Tranquil Trader

Price-Forecasting Models for MutualFirst Financial Inc. MFSF Stock (NASDAQ Composite Components, #1795)

by Ton Viet Ta

Price-Forecasting Models for Ark Restaurants Corp. ARKR Stock (NASDAQ Composite Components, #773)

by Ton Viet Ta

Crisis and Sequels (Studies in Critical Social Sciences, #109)

As the economic crash of 2007-8 and its sequels developed, neoliberal economists often said that economic theory can never cope with such eruptions, and left-minded economists and political economists struggled to find answers. This book documents discussions as they developed; an introduction and an afterword tell the story of the crisis, and offer syntheses and angles on some of the debated issues. What were the chief imbalances in the world economy? Is US hegemony breaking down? Were falling...

16 Candlestick Patterns that Every Trader Should Know

by Anthony McAllen

Price-Forecasting Models for Cohen and Steers Total Return Realty Fund RFI Stock

by Ton Viet Ta

Finite Difference Methods in Financial Engineering (Wiley Finance, #312)

by Daniel J. Duffy

The world of quantitative finance (QF) is one of the fastest growing areas of research and its practical applications to derivatives pricing problem. Since the discovery of the famous Black-Scholes equation in the 1970's we have seen a surge in the number of models for a wide range of products such as plain and exotic options, interest rate derivatives, real options and many others. Gone are the days when it was possible to price these derivatives analytically. For most problems we must resort t...

Price-Forecasting Models for Invesco Van Kampen Bond Fund VBF Stock

by Ton Viet Ta

Price-Forecasting Models for Tidewater Inc TDW Stock

by Ton Viet Ta

Price-Forecasting Models for DLH Holdings Corp. DLHC Stock (NASDAQ Composite Components, #1208)

by Ton Viet Ta